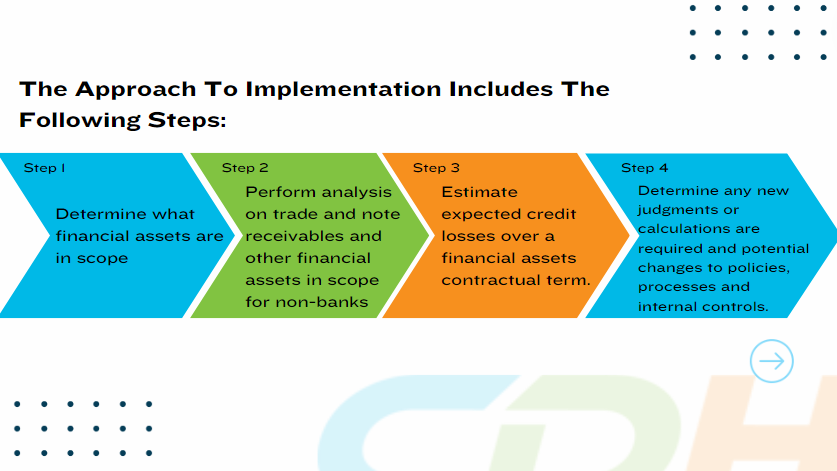

CECL stands for Current Expected Credit Loss, and it refers to a new accounting standard introduced by the Financial Accounting Standards Board (FASB) for estimating credit losses on financial instruments. While banks and financial entities will be most impacted by the new model, what about non-financial institutions? These implementations for non-financial companies with certain financial instruments, including trade receivables, will impact how credit losses are estimated. Check out this graphic below on our straightforward steps for implementation:

Here are some key steps and considerations for implementing CECL:

Step 1: Determine what financial assets are in scope

Review the listing of those financial assets in scope and compare to entities balance sheet and other arrangements

Step 2: Perform analysis on trade and note receivables and other financial assets in scope for non-banks

Group assets/customers with similar risk characteristics into a pool for evaluation.

Determine the method for measuring losses and analyze.

Step 3: Estimate expected credit losses over a financial assets contractual term.

Determine the impact to the financial statements, if any – allowance for credit losses

Update disclosures related to adoption

Step 4: Determine any new judgments or calculations are required and potential changes to policies, processes and internal controls

What needs to be included in the existing process to calculate on an ongoing and periodic basis.

It’s important for companies to work closely with their accounting teams, risk management teams, and possibly advisors to ensure a smooth and accurate implementation of CECL. Additionally, staying informed about updates and guidance from regulatory bodies is crucial in maintaining compliance with accounting standards.